PJM Warns of Winter Supply Crunch as Data Center Power Demand Soars

A surge in power demand from data centers is pushing the nation’s largest electricity market toward a winter supply crunch, extending a rally in renewable energy contracts while prompting warnings from the grid operator.

PJM, operator of the competitive wholesale market spanning the mid-Atlantic and Midwest, forecasts that peak power consumption this winter will reach 145,700 MW, representing an all-time high for the season. This load growth is driven primarily by energy-intensive data centers by tech giants Amazon, Google, and Microsoft. Their spending on such hubs hit a record $40 billion in June, with much of those investments in PJM states.

The explosive demand is leaving supply behind. With 1,000 MW of new dependable capacity added since last winter, mostly from solar, PJM’s reserve margin – the critical buffer for meeting peak demand – is expected to shrink by 14% from last winter. This is expected to create conditions ripe for price spikes and supply shortfalls.

“The tightening of our margins will begin to impact us in the next few years if it continues,” said Aftab Khan, PJM’s executive vice president of operations, planning and security, in a statement on Nov. 3. “PJM is working on multiple levels with all of our stakeholders to reverse this trend of demand growing faster than we can add generation.”

For PJM’s renewable sector, the winter outlook provides fresh evidence of the market’s worsening supply shortage. The unrelenting load growth, with the prospect for more frequent high and extreme pricing, is translating into higher power forwards, which is a key component in renewable valuations. Consequently, wind and solar contract values are now reaching levels not seen in at least a year.

The fair market value for a 10-year as-generated wind PPA for delivery in PJM’s benchmark Western hub reached $89.34/MWh on Nov. 14, up by nearly 3% from the start of October, and just shy of the 12-month high.

According to the U.S. Energy Information Administration’s (U.S. EIA) latest Short-Term Energy Outlook, the amount of energy required to meet load, including imports, is projected to reach about 906 million megawatt-hours next year, up 8.9% from 2024.

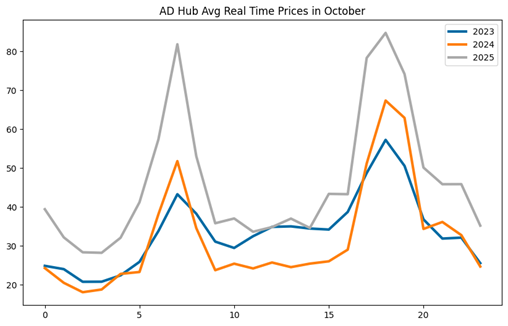

The elevated demand is not only occurring across seasons but across all hours of the day. For example, in October in the AEP Dayton hub average around-the-clock prices were approximately 50% higher and system-wide demand was 2 terawatt-hours more compared to the same period in 2024, according to an analysis by Pexapark.

Other market pressures are compounding the issue. Surging LNG exports, set against flat natural gas production, are expected to push gas prices higher. This will have an outsized impact on the gas-heavy PJM market where gas-fired generators set the price of power most of the time. As a result of the higher fuel prices, wholesale power prices in the Western Hub are forecast to reach a four-year high of $60.88/MWh in 2026, according to the U.S. EIA.